Your Gas Price Is Set by a Ship That Sailed in February. Twenty percent of the world's oil moved through one narrow strait. Then the shooting started. The ships that got out are almost here. What comes after them is the question.

At a glance: In the weeks following the U.S.-Israel joint strikes on Iran on February 28, 2026, the Strait of Hormuz, the narrow chokepoint through which roughly twenty percent of the world's daily oil supply flows, was effectively sealed to Western-affiliated shipping. Tanker traffic that once averaged more than a hundred vessels per day fell to near zero almost overnight. The oil that was already at sea when the shooting started is arriving now. After those ships dock, there is nothing behind them, and the world is about to feel what that means.

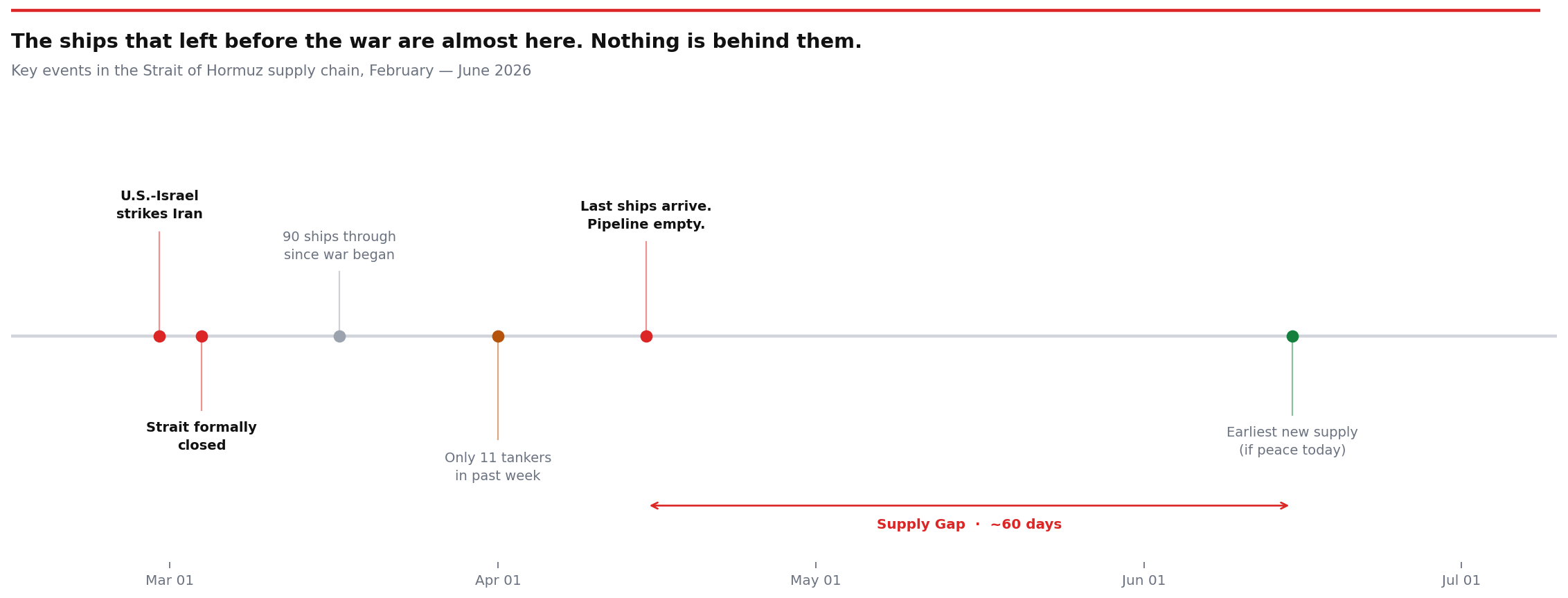

How we got here: On February 28, 2026, the United States and Israel launched coordinated strikes on Iran, killing Supreme Leader Ali Khamenei. The strikes were swift. The consequences were not. Within days, Iran moved to close the Strait of Hormuz to any vessel with Western affiliations, formalizing the blockade by March 4. The Strait is a body of water roughly 33 kilometers wide at its narrowest point, sitting between the Arabian Peninsula and the Iranian coast. It is, by any reasonable measure, one of the most consequential pieces of ocean on the planet. About 20 million barrels of oil pass through it every single day, serving refineries across Europe, Asia, and North America. When it closed, the world's oil system did not immediately collapse. It began to drain, slowly and with the particular cruelty of a slow leak rather than a sudden break.

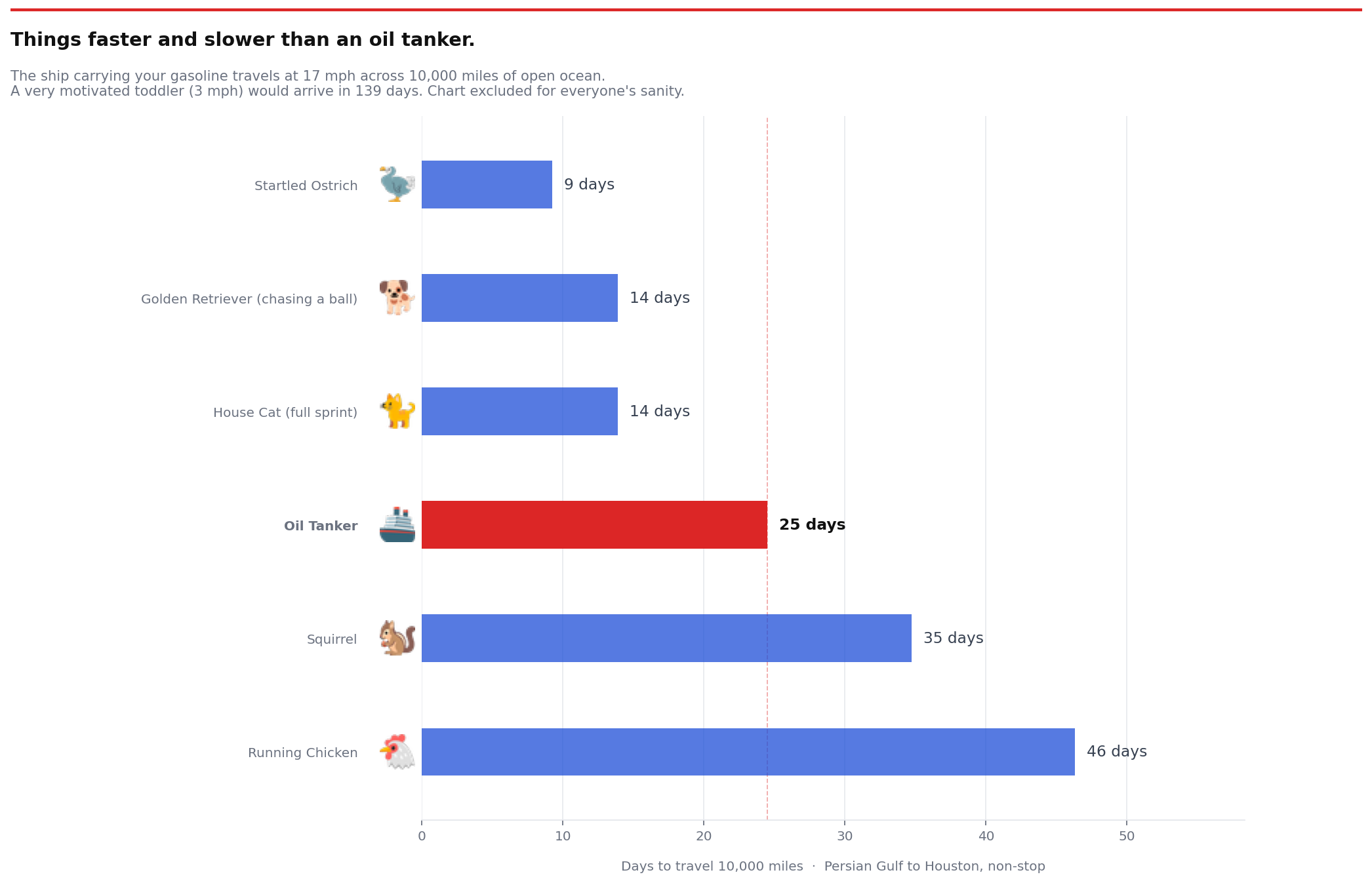

The geography of speed: To understand why this crisis unfolded over weeks rather than hours, you need to understand how oil actually moves across oceans. Tankers are enormous, efficient, and extraordinarily slow. A typical Very Large Crude Carrier cruises at somewhere between 13 and 17 knots, which translates to roughly 15 to 20 miles per hour. A car merging onto the highway moves four to five times faster. These are not vessels that can sprint to make up lost time. And because of this, the voyage from the Persian Gulf to the United States East or Gulf Coast takes anywhere from 35 to 60 days depending on routing, weather, and the specific destination port. That distance, measured in time rather than miles, is the central fact of this entire crisis. It means that decisions made on the water in early March will not show up at American refineries until April or May. And decisions made today, or not made today, will shape what those refineries are running on in June and July.

The ships already moving: When the strikes happened and the Strait began to close, some tankers were already in the water, already past the chokepoint, already on their way. As of March 17, roughly 90 vessels had slipped through the strait since the conflict began. These were ships that moved fast in the earliest, most ambiguous window of the crisis, before insurance markets froze and before ship operators fully understood the risk environment. By April 1, however, only 11 tankers had transited the strait during the entire previous week, and 71 percent of those transits were conducted by Iranian shadow fleet vessels, not ships carrying oil bound for Western markets. Shadow fleet ships, older tankers operating outside conventional insurance and tracking systems, now account for 88 percent of all strait transits. The ships that left before the war are the ones keeping Western markets supplied right now. They will not be supplying them much longer.

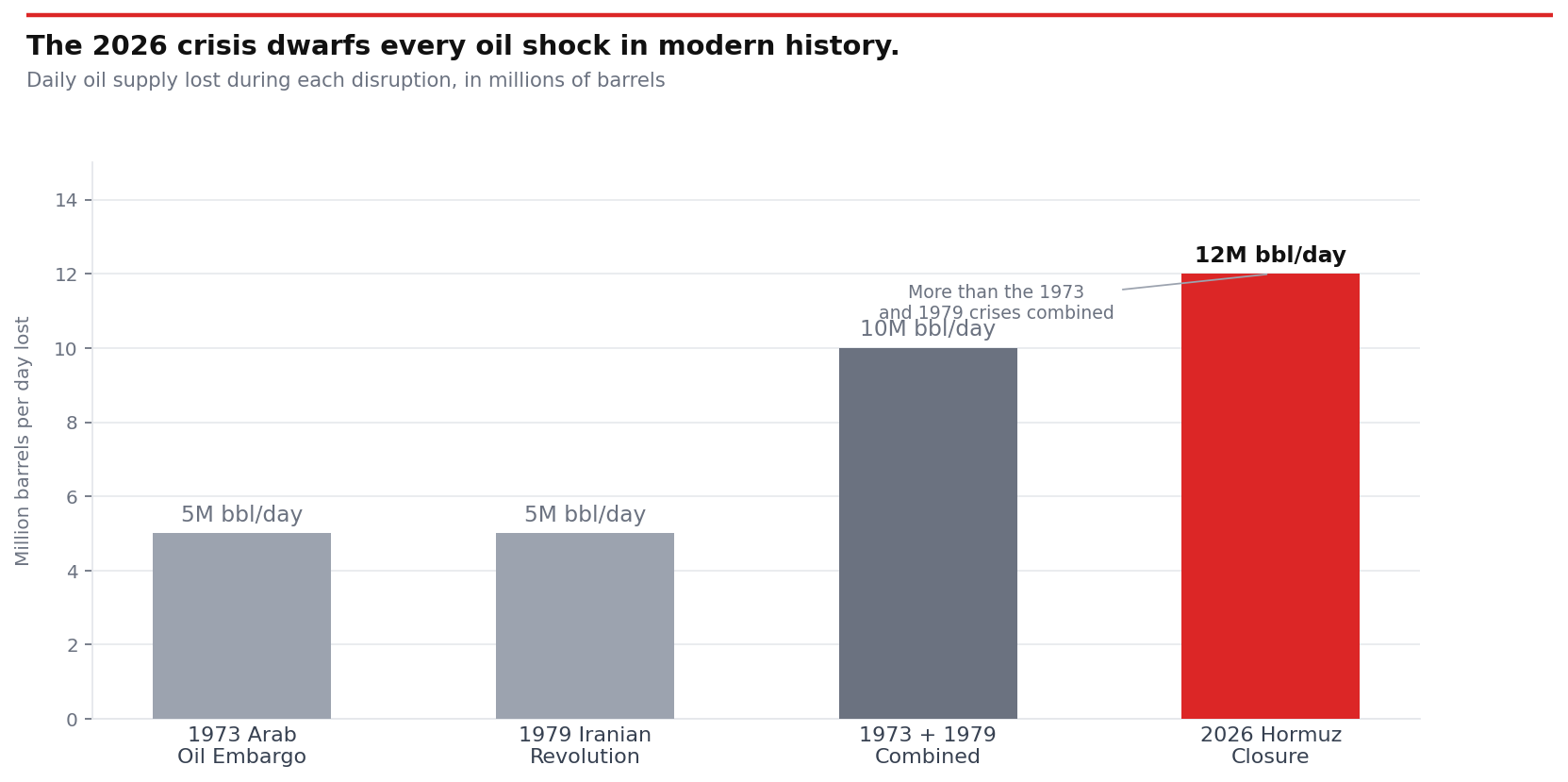

The April 15 moment: International Energy Agency Director Fatih Birol was direct when he addressed reporters: "April is going to be far worse than March." The logic behind that statement is not complicated, but it is worth following carefully. The ships that were at sea in late February, already loaded and already moving, are arriving now. They represent the trailing edge of the pre-crisis supply pipeline. Once they dock and offload, there is nothing behind them. The IEA has warned that the oil shortfall in April will be roughly double what it was in March. To put that in context, the world is already losing an estimated 12 million barrels per day, a figure that exceeds the supply disruptions of both the 1973 Arab oil embargo and the 1979 Iranian Revolution, combined. The most consequential date in this supply chain is approximately April 15. That is when, by most transit-time calculations, the last of the ships that departed the Gulf before or immediately after the conflict began will have arrived at their destinations. At that point, the cupboard goes bare. U.S. refineries will begin drawing down strategic reserves without any new tanker arrivals scheduled to replace what they consume.

What the price signals are saying: Markets registered the severity faster than policy did. Brent crude surged more than 60 percent in March alone, hitting a peak of $126 per barrel. At the pump, Americans crossed a threshold that carried its own psychological weight: the national average price for regular gasoline broke $4 per gallon for the first time since 2022. Those numbers reflect what futures traders believe about near-term supply, and right now, what they believe is that supply is going to get tighter before it gets better. Oil markets have an uncomfortable tendency to front-run physical reality, pricing in anticipated scarcity before consumers actually feel it in a meaningful way. What is coming in April and May is the physical reality catching up to what prices have already signaled.

The reserve release: In response to the shortfall, the IEA approved an unprecedented coordinated strategic reserve release of 400 million barrels across its member nations. The United States is contributing 172 million barrels of that total. At the maximum draw rate of 4.4 million barrels per day, the American release buys roughly 40 days of supplemental supply. It will push Strategic Petroleum Reserve levels down to approximately 243 million barrels, the lowest level since the early 1980s. Birol was careful about expectations: "This merely alleviates the immediate discomfort. It is not a solution. The real solution lies in reopening the Strait of Hormuz." The reserve release is a bridge, not a destination. It is designed to prevent a hard cliff in supply from becoming a catastrophic disruption, but it does not address what happens when the 40 days are up and the strait is still closed, or what happens when the U.S. eventually needs to replenish reserves it has drawn to historic lows.

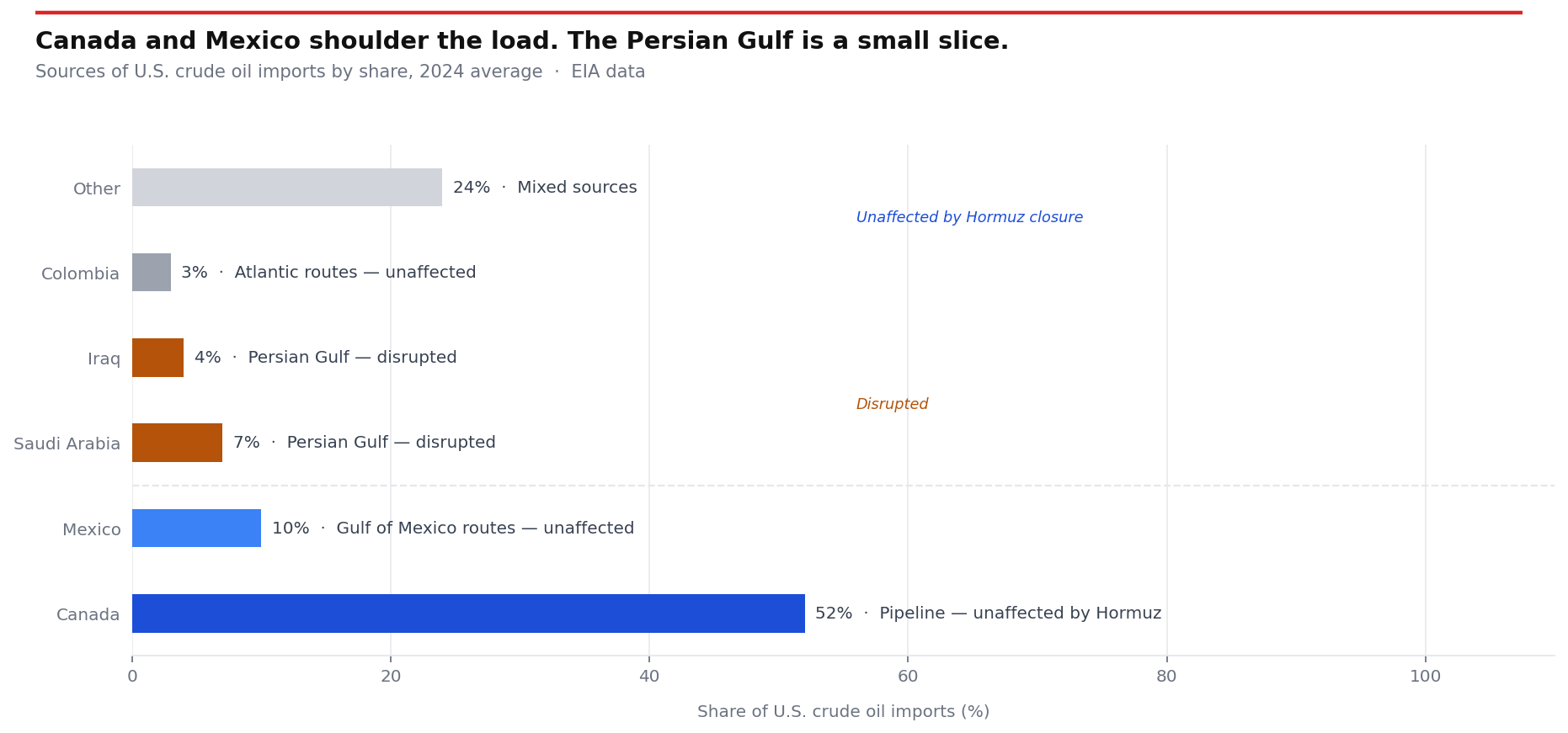

Where else the oil comes from: The United States is not entirely dependent on Persian Gulf crude, and the crisis has thrown into sharp relief the parts of its import network that are not affected by the Hormuz closure. Canada is by far the largest single source of foreign crude for the U.S., supplying 52 percent of all imports via pipeline systems that have nothing to do with ocean shipping or the Middle East. Mexico supplies another 10 percent via comparatively short routes across the Gulf of Mexico. The U.S. itself is the world's largest oil producer, and domestic shale and tight oil production can be scaled, though doing so takes weeks to months, not days. The more politically complicated piece of the supply puzzle is Venezuela. Before the reimposition of broad U.S. sanctions in 2019, Venezuelan heavy crude accounted for up to 800,000 barrels per day flowing into Gulf Coast refineries, many of which were specifically designed and configured to process that particular grade of oil. Redirecting existing Venezuelan exports is relatively fast. Ramping Venezuelan production back to pre-decline levels would take years, and doing so would require a significant shift in U.S. foreign policy. None of these alternatives, taken together, fully replace what came through the Strait.

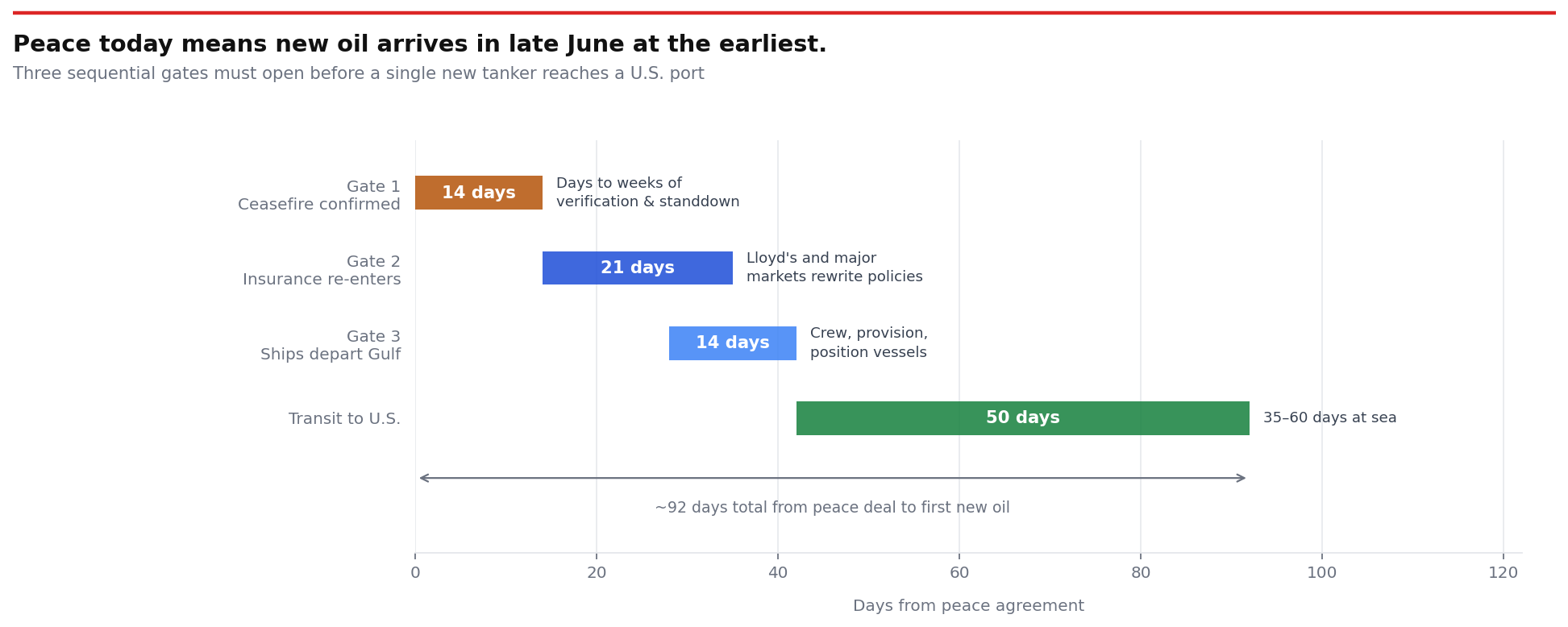

If peace was reached today: It is worth being precise about what a ceasefire, even a successful one, actually does to the oil supply timeline. The answer is less than most people assume, and certainly not immediately. Even with a signed peace agreement today, ships do not begin moving tomorrow. There are three sequential gates that must open before a single new tanker can depart the Persian Gulf for the United States. The first is ceasefire confirmation, which takes days to weeks depending on the complexity of the terms and whether Iranian naval authorities formally stand down the closure. The second is insurance re-entry. Lloyd's of London and the major marine insurers that have effectively exited the region will need time to reassess the risk environment, update their war-risk coverage, and begin writing policies again. That process takes one to three weeks. The third is ship operator re-engagement. Once a vessel has insurance coverage and a cleared legal path, the operator still needs to crew, provision, and position the ship. A realistic timeline from a signed peace deal to the first new tanker actually departing the Persian Gulf is two to four weeks. Then add the voyage itself: 35 to 60 days from the Gulf to the U.S. Gulf or East Coast. A peace agreement signed today means new Gulf oil does not reach American shores until mid-June to early July 2026 at the earliest. The total gap between now and any meaningful normalization of physical supply is 75 to 90 days. Gas prices above $4 per gallon are likely to persist through at least July, even in the most optimistic scenario. The SPR draw will also put a price floor under crude for the remainder of the year, as the government eventually needs to buy oil to replenish reserves it has now drawn to their lowest levels in roughly four decades. Markets will price that future demand accordingly.

The slowest kind of crisis: What makes this crisis so difficult to absorb politically and psychologically is that it does not arrive all at once. It has been arriving in stages, at tanker speed, for five weeks now. The strikes happened in a day. The closing of the strait happened over a few days. The drain on the supply pipeline has been happening for a month. The hardest impact is still arriving. This is not a hurricane that makes landfall and then passes. It is a slow-motion sequence of consequences, each one following from decisions made weeks ago, each one now largely beyond the reach of any single day's policy choices. The ships that left before the war are almost here. The question that matters now is not what happened in February, but what will be moving through any open straits in May, and whether there will be enough of it.

SOURCES: cnbc.com, apnews.com, en.wikipedia.org, reuters.com, thenation.com, cbsnews.com, openthemagazine.com, ainvest.com, theconversation.com, ktvu.com, atlanticcouncil.org, tbsnews.net, eia.gov

BigEV Members enjoy significant savings and special access on tens of thousands of independent energy products, parts, accessories, jobs and talent across hundreds of categories, all in one global marketplace.