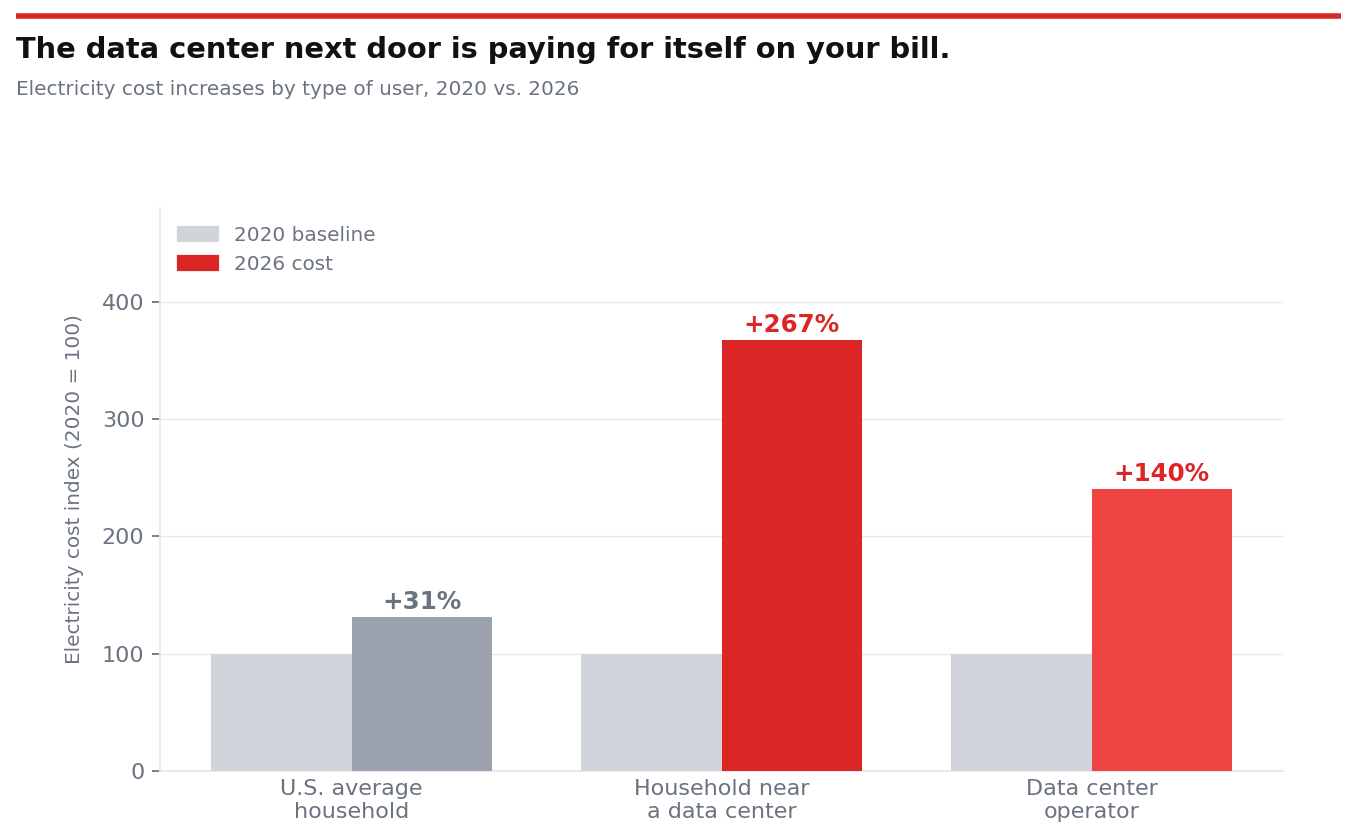

At a glance: Before the Strait of Hormuz closed, America's AI data centers were already in an energy crisis of their own making. Electricity costs had risen 31 percent between 2020 and 2025, capacity prices in the mid-Atlantic grid had surged 833 percent in two years, and communities near large data center campuses were paying electricity bills up to 267 percent higher than they had five years earlier. Then the war arrived. Diesel shortages are now projected to reach the United States by April or early May 2026, hitting the one fuel that every data center depends on as its final insurance policy. At the same time, tariffs on steel, aluminum, copper, and chips are layering hundreds of millions of dollars in new costs onto a sector that was already absorbing punishing price increases. Demand for AI compute has not slowed. What has changed is what it costs to keep the lights on.

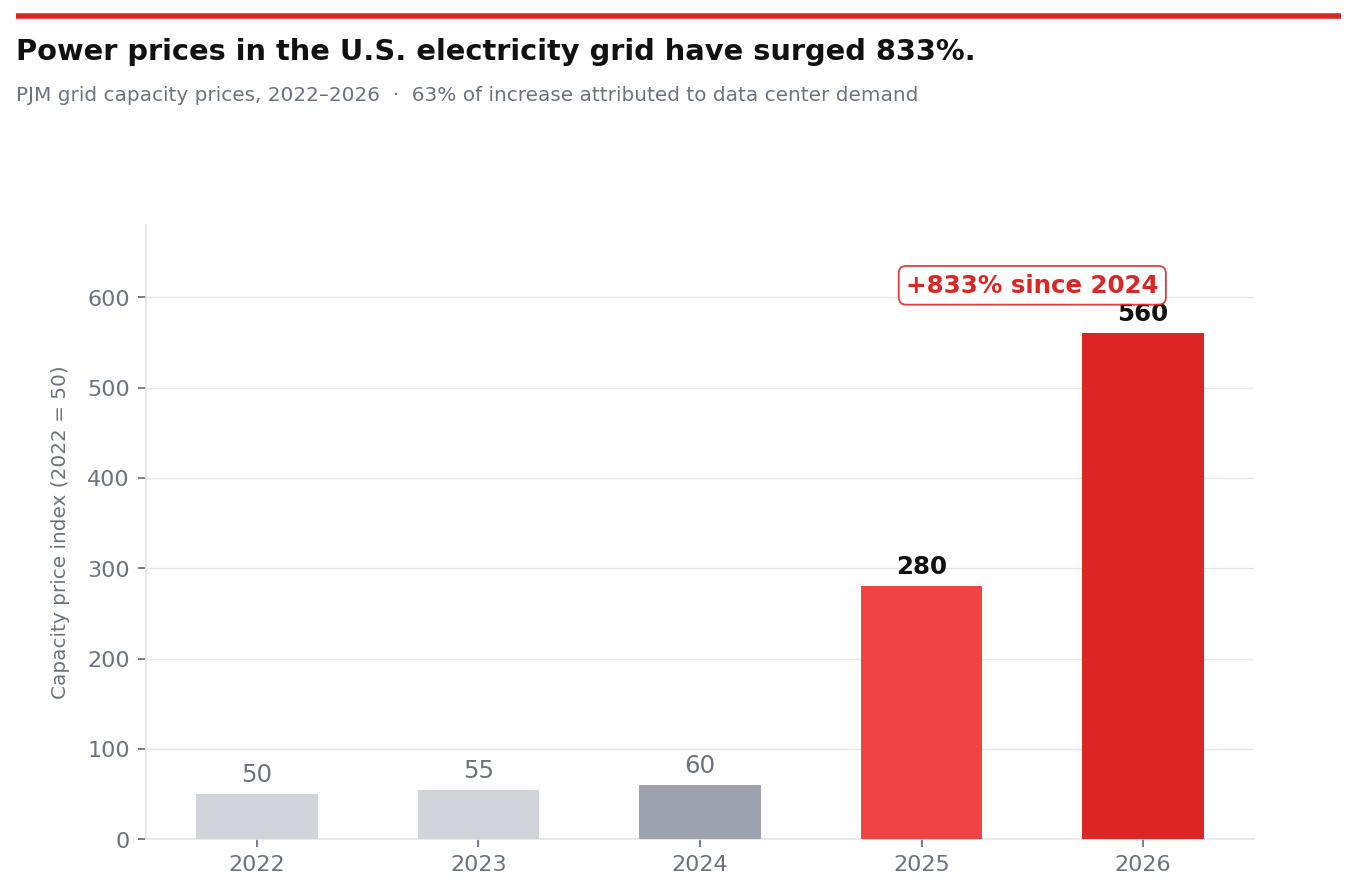

The power problem was already here: The data center industry did not wait for a geopolitical crisis to create an electricity problem. U.S. electricity costs rose 31 percent between 2020 and 2025, compared with just 4 percent in the five years before that. Data centers account for 40 percent of all electricity demand growth in the country, and Goldman Sachs has projected they will raise core inflation by 0.1 percent annually through 2027. In the PJM interconnection, the grid that serves much of the mid-Atlantic and Midwest, capacity prices surged 833 percent from 2024 to 2026, with analysts attributing 63 percent of that spike to data center demand alone. A single hyperscale facility can consume as much electricity as 2 million U.S. homes. The United States is home to 5,427 AI-related facilities, roughly 45 percent of all data centers on earth, and the GPU racks inside them consume 2,000 watts or more each, ten times the draw of a traditional CPU rack. Communities that happened to be near these campuses were already paying electricity bills up to 267 percent higher than in 2020. The crisis, in other words, was structural before it was geopolitical.

Then the war arrived: Natural gas is the primary fuel powering most U.S. data centers, and the closure of the Strait of Hormuz upended the global natural gas market almost immediately. The effects on American domestic gas prices have been more contained than in Europe or Asia, where the disruption has been acute, but no large energy market is an island. Prices have risen, supply chains for liquefied natural gas have been rerouted, and the marginal cost of generating electricity from gas has climbed with it. For data center operators who had already spent years negotiating long-term power purchase agreements at fixed rates, the exposure feels manageable. For those buying power on the spot market, the war made a difficult situation considerably worse.

The generator in the room: Diesel is not how data centers run. It is how they survive when everything else fails. Every major facility maintains banks of diesel generators as its backup power source, the infrastructure behind the "five nines" uptime guarantee that enterprise customers pay for and that cloud service contracts legally require. Without functioning diesel backup, that guarantee collapses. The IEA has warned that diesel and jet fuel shortages will reach the United States by April or early May 2026. In Texas, where ERCOT can already force large users offline during peak demand periods, some data centers have started running their diesel generators more frequently than backup infrastructure was ever designed to handle. The generators are being used not as a last resort but as a supplement. That changes maintenance schedules, fuel consumption contracts, and operating costs in ways the industry did not model.

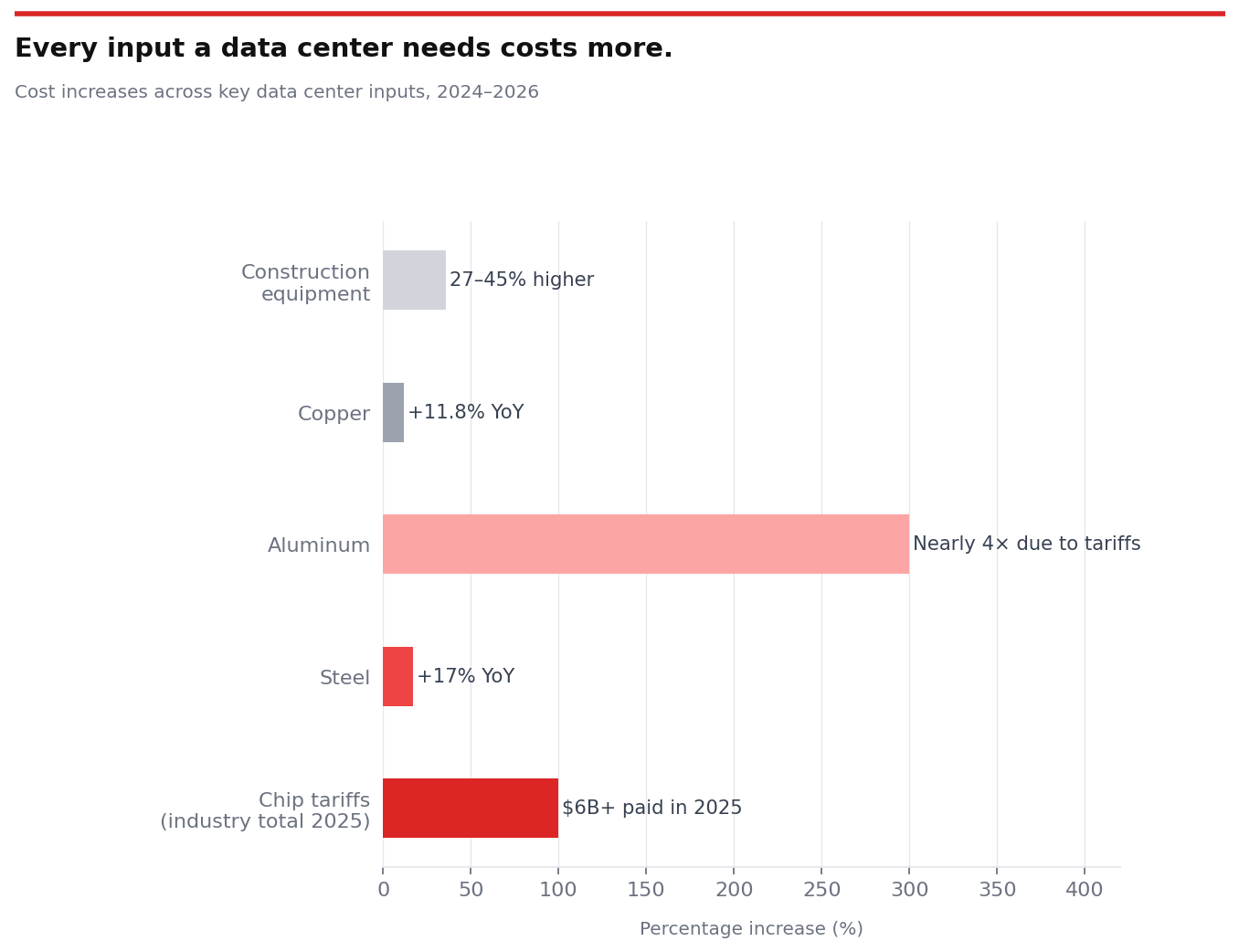

What it costs to build one: A data center under construction today is absorbing cost shocks from two directions at once. Steel tariffs were already at 50 percent heading into 2026, and steel mill products jumped 17 percent in 2025 alone. Aluminum, a core material in data center cooling and structural systems, has nearly quadrupled in cost in the U.S. due to tariffs. Copper climbed 11.8 percent year over year. Construction equipment costs are 27 to 45 percent higher depending on where the equipment was manufactured. A single $375 million data center project now faces an estimated $22 million in additional costs attributable purely to tariffs. Project abandonment rose 88.2 percent year over year across commercial construction, and 43 percent of contractors report cancellations or delays directly caused by high material costs.

The chip problem nobody is talking about: AI data centers paid more than $6 billion in tariffs on hardware in 2025 alone. A single high-end AI rack can cost $3 to $4 million, with the chips inside representing 70 to 80 percent of that bill. DRAM, high-bandwidth memory, and GPUs are committed and allocated through the late 2020s. South Korean chip manufacturers SK Hynix and Samsung supply most of the world's high-bandwidth memory, and a meaningful portion of the industrial helium they depend on for chip fabrication comes from the Middle East, a supply chain now disrupted by the war. Hard drives from Western Digital are being quoted to customers with lead times stretching to 2027. There is one significant buffer: chips manufactured by TSMC in Taiwan remain duty-free when imported as assembled boards. Whether that exemption survives the next round of trade negotiations is a different question.

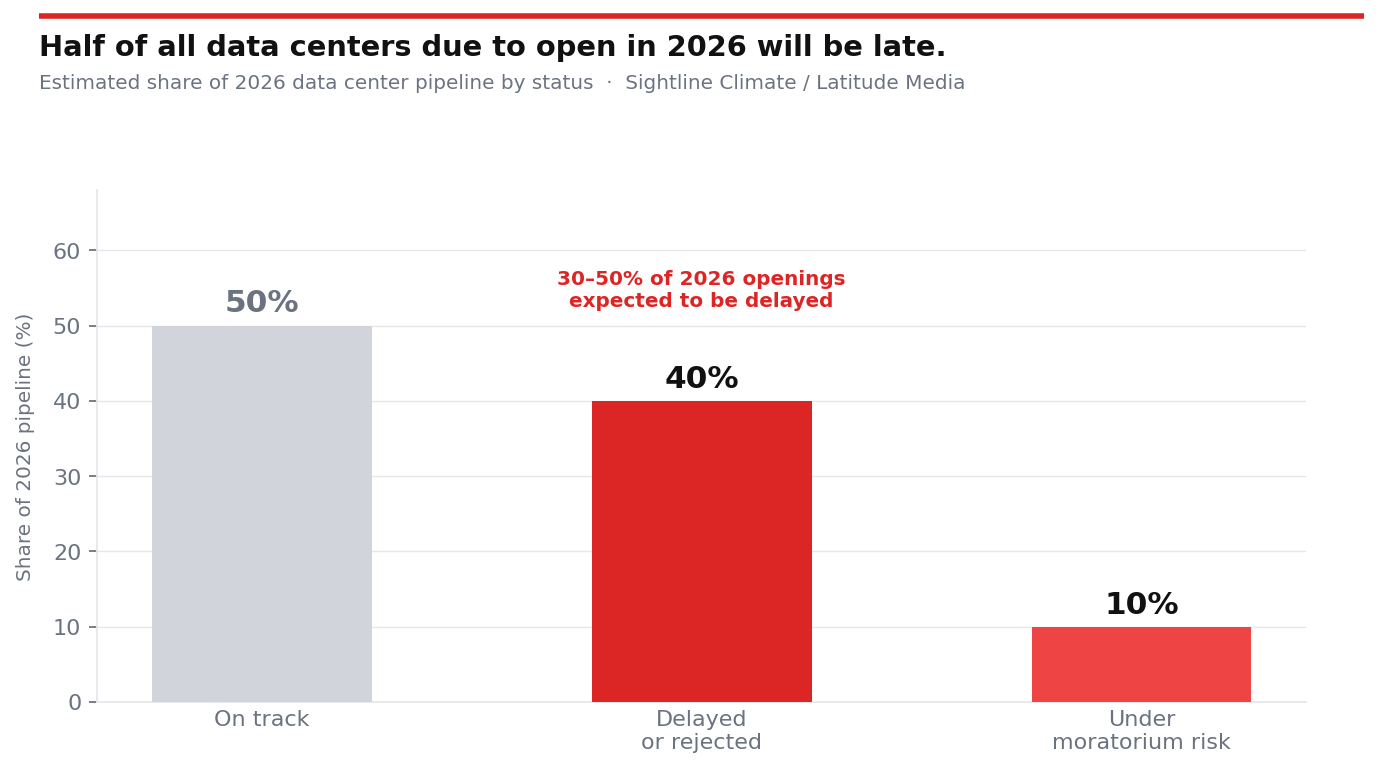

Has construction actually stopped?: Not stopped. But bent. Between 30 and 50 percent of all data centers scheduled to open in 2026 are expected to be delayed. At least $162 billion in data center investments have been affected by delays or project rejections since 2024. The paradox is that demand for AI compute has not softened, which means hyperscalers are making a calculated choice to absorb higher costs rather than slow construction. The bet they are making is that the AI arms race will outlast the financial pressure. So far, the bet is holding. But the cracks are forming.

The politics caught up: On March 25, 2026, Senator Bernie Sanders and Representative Alexandria Ocasio-Cortez introduced the AI Data Center Moratorium Act, a bill calling for a complete national pause on new data center construction. In the first six weeks of 2026, more than 30 states filed over 300 bills related to data center regulation. New York has proposed a three-year halt on all new construction. Michigan, South Dakota, and Oklahoma all have active moratorium bills. Voters in communities near data centers have watched their electricity rates rise as much as 267 percent since 2020. Data centers, which were once a largely invisible piece of infrastructure, are now a kitchen-table issue.

The global realignment: The Middle East was supposed to be the next frontier of hyperscale AI investment. The UAE and Saudi Arabia had announced significant AI campus projects. The war has put those plans on hold, inflating any regional data center CAPEX by 15 to 20 percent. The one counterintuitive beneficiary may be U.S.-based data center development. American domestic natural gas is relatively insulated from the Hormuz crisis compared with Europe and Asia. For global investors looking to site new AI infrastructure in a location with stable power costs, the United States may actually become more attractive precisely because the rest of the world's energy situation is more fragile.

The arms race doesn't stop: Oil prices hit operating costs directly. Natural gas is more expensive globally. Steel and aluminum are up 17 to 30 percent or more. GPUs and memory are tariffed, constrained, and allocated through 2028. PJM capacity pricing has risen 833 percent. Consumer electricity bills in data center communities are up 267 percent compared to 2020. And yet demand for AI compute has not cooled. The companies building these facilities understand that the infrastructure they lock in today will determine market position for the next decade. A one-year delay to save $200 million is not a good trade if it means falling behind a competitor who did not delay. So the construction continues, the generators run, and the electricity bills go up. The oil crisis hits twice: once at the pump, and once on the electricity bill that powers the AI that is already running your life.

Sources: cnbc.com, fortune.com, multistate.us, latitudemedia.com, thecooldown.com, aljazeera.com, datacenterknowledge.com, marketplace.org, enkiai.com, forbes.com, agc.org, insideclimatenews.org, americandouglasmetals.com, spglobal.com

BigEV Members enjoy significant savings and special access on tens of thousands of independent energy products, parts, accessories, jobs and talent across hundreds of categories, all in one global marketplace.